Uncovering Payment Fees: Scheme, Interchange, Processing Fees, and More.

Uncovering Payment Fees: Scheme, Interchange, Processing Fees, and More

By Rihab Oudda (July 31, 2025)

Payments are a fundamental aspect of any business, touching nearly every department—Finance, Accounting, Operations, and dedicated Payment teams. Yet, despite their critical role, the true cost of payment processing remains elusive for many organizations. Transparency in payment fees is vital because, for many businesses, these costs for some businesses can rank as the second-highest expense after employee salaries. Understanding the full scope of payment processing fees empowers businesses to optimize operations, improve profitability, and make informed strategic decisions.

The total cost of processing payments extends far beyond the basic interchange and scheme fees outlined in contracts. Especially in models like Interchange++, numerous transaction-specific factors, such as card type, transaction method, and risk profile, can significantly impact pricing. Uncovering these hidden costs is essential for businesses to ensure they’re not overpaying and to maximize their bottom line.

Who’s Involved in a Transaction

Every card payment involves a complex network of parties, each taking a cut or adding to the overall cost:

- Issuer: The bank or financial institution that issues the card to the consumer, charging interchange fees to offset the risk of extending credit or debit services.

- Acquirer: The merchant’s bank or financial institution that processes card payments and facilitates settlement, often charging a premium for its services.

- Card Network: Entities like Visa, Mastercard, or American Express, which manage the payment infrastructure and charge scheme/assessment fees for network access and risk tools.

- Payment Processor/Gateway: Intermediaries that handle transaction processing, charging fees for their technology and services.

Each participant in this ecosystem contributes to the Merchant Discount Rate (MDR), the total cost of accepting a card payment, which, on average, will be a cost between 1 and 3% for low-risk businesses.

The Main Categories of Payment Fees

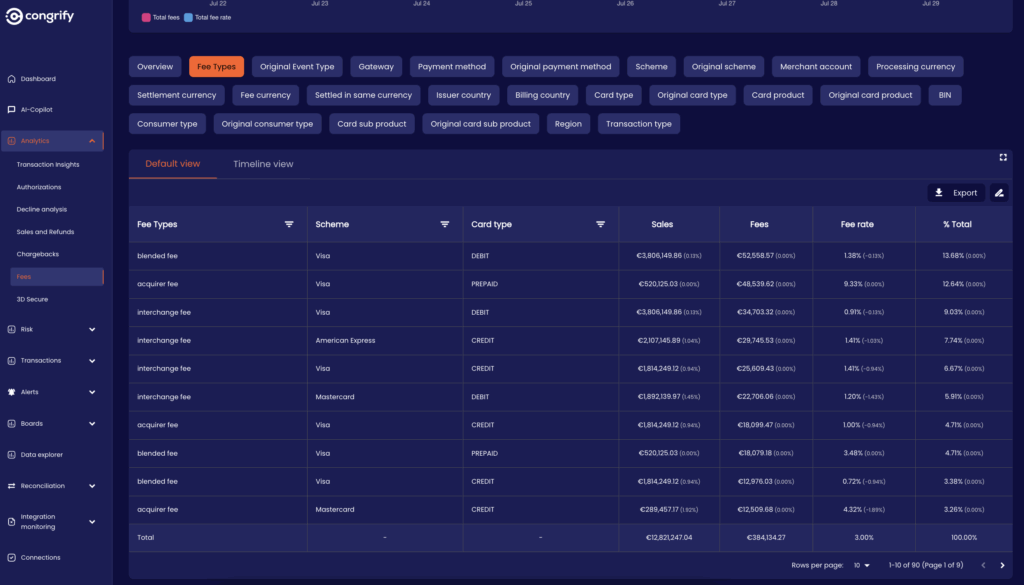

Understanding the full spectrum of payment-related charges is essential for transparency, costs reconciliation, optimization and the overall correct fee allocation on a transactional level. Below are the core fee categories:

-

Interchange Fees

Paid to the card issuer. Rates vary by card type, transaction method, and geography (e.g., consumer vs. corporate cards). Often, the largest component of MDR.

-

Scheme Fees

Charged by card networks (Visa, Mastercard, etc.) to cover infrastructure, transaction processing, fraud, authentication and risk tools.

-

Acquirer Premiums

A markup by acquiring banks based on merchant business model, merchant category code, risk profile, volume or associated settlement services.

-

Gateway Fees

Typically charged by a PSP, a payment orchestrator, an e-commerce or a subscription platform to offer a checkout infrastructure, initiate transactional API calls and communicate with the acquirers.

-

Chargeback Fees

A flat fee per dispute, covering administrative costs. Frequent chargebacks can lead to higher risk premiums.

-

Currency Conversion Fees

Cross-border payments can trigger FX markups and international service fees.

-

Terminal and Hardware Costs

Applicable in card-present environments. Includes POS terminals, mobile readers, or hardware rentals.

-

Risk management fees

Fees associated to stand-alone risk engines or authentication services such as 3D Secure.

-

Other Fees

- Tokenization Vaults for securing card data

- PCI Compliance Fees for adhering to data protection regulations

- Monthly Statement or Setup Fees charged by some processors

- Shopping Cart Integrations, which may include platform usage fees

Even a single transaction can incur multiple-layered charges, depending on how it’s processed.

Common Pricing Models Explained

Payment service providers offer various pricing models, each with distinct advantages and trade-offs. Selecting the right model depends on your business size, transaction volume, and operational needs. Below, we explore the most common models, highlighting how they reveal or obscure true costs.

Flat Rate and Blended Pricing

In flat-rate or blended pricing, all fees (interchange, scheme, processor, and gateway) are combined into a single rate, typically in a price range between 2 and 3% plus a fixed transactional fee. This model is ideal for small businesses or startups due to its simplicity and predictability.

Pros:

- Simplicity: A single rate makes budgeting straightforward, with no need to dissect complex fee structures.

- Predictability: Merchants can easily estimate costs, especially for low transaction volumes.

- Good for Startups: Allows new businesses to focus on operations without delving into fee intricacies.

Cons:

- Lack of Transparency: Merchants don’t see the breakdown of interchange or scheme fees, potentially overpaying for low-cost transactions like debit card payments.

- Higher Costs for Low-Value Transactions: The fixed per-transaction fee ($0.30) can significantly increase costs for small-ticket items ($20 or less).

- Limited Flexibility: Rates are often non-negotiable unless the business achieves high sales volumes.

Subscription (SaaS-Style Payment Processing)

Offered for example by gateways focused on subscription-based models, charging a fixed monthly fee plus lower per-transaction rates. This is less common but suits businesses with high transaction volumes — such as subscription management platforms — seeking predictable costs.

Pros:

- Cost Predictability: Fixed fees make budgeting easier for high-volume businesses.

- Good for Startups: Allows new businesses to focus on operations without delving into fee intricacies.

Cons:

- Higher Costs: Monthly fees can be expensive for businesses with inconsistent transaction volumes and result in higher costs.

- Complex Integration: May require more setup effort compared to flat-rate models.

Interchange Plus (Interchange++)

Interchange++ (or pass-through) pricing is the most common model for enterprise merchants. It separates fees into interchange, scheme, and processor/gateway components, with the processor adding a fixed markup. The total rates would still include a fixed transaction fee and then a margin that is specified only on the acquiring side, as the other fees such as interchange and scheme fees are pass-through, therefore variable depending on the card types and the processing regionality or characteristics.

Pros:

- Transparency: Merchants see exactly what each party (issuer, network, processor) charges per transaction.

- Lower Costs: Often more cost-effective than blended rates, especially for high-volume businesses, with potential savings of >1% per transaction when optimized as a cost setup.

- Negotiable: Processors may adjust their markup for high-value or low-risk merchants.

Cons:

- Complexity: Varying rates per transaction make cost prediction challenging.

- Operational efforts: More efforts in tracking and analyzing fee items to look for the best optimization strategies.

- High Interchange for specific Cards: Cards like commercial or premium ones can carry interchange costs of more than 2%

Regional & Industry-Specific Influences

Payment processing fees vary significantly by region and industry, driven by regulatory frameworks, risk profiles, and transaction characteristics.

EU vs. US Interchange Caps

In the EU, interchange fees are capped under the Interchange Fee Regulation (IFR), limiting consumer debit card fees to 0.2% and consumer credit card fees to 0.3% for intra-European transactions. These caps reduce costs for merchants but don’t apply to commercial transactions, where commercial cards are subject to a higher cap.

In the U.S., the Durbin Amendment regulates debit card interchange fees for large issuers—banks and credit unions with more than $10 billion in assets. For card-present transactions, the maximum interchange fee is capped at 0.05% of the transaction amount plus $0.21.

In contrast, credit card interchange fees and debit fees from exempt issuers (smaller banks) are not capped and typically range from 1.15% to 3.15% plus $0.04 to $0.25, depending on the transaction type, processing method, and merchant category. For detailed EU and US interchange rates, visit Congrify’s Knowledge Hub.

High-Risk Industries

Industries like travel, gaming, or crypto face higher fees due to elevated chargeback risks. While interchange and scheme fees remain consistent, acquirers often charge higher premiums to account for potential disputes, influenced by the merchant’s Merchant Category Code (MCC).

Beyond regional regulations and risk profiles, merchant costs also increase based on customer behavior and business setup. Businesses with high cross-border volumes often face higher scheme and interchange fees, especially when processing foreign-issued cards. Similarly, if your customer base includes many corporate or commercial card users, you’ll see elevated interchange rates compared to standard consumer debit cards.

Expanding into multi-region markets also means integrating local payment methods—from wallets to Buy Now Pay Later (BNPL) solutions. While essential for conversion, these options often come with premium fees, since they typically involve credit risk and installment financing managed by the provider.

Checklist: 10 Practical Ways to Reduce Your Payment Fees

We have summarized below a check-list with 10 steps to follow for payment fees optimization depending on the type of your business and your transaction processing strategy:

- Use multiple PSPs to gain flexibility and negotiation power

- Enable local acquiring to reduce cross-border and network fees

- Encourage lower-cost payment methods (e.g. ACH, SEPA, Pix, iDEAL)

- Optimize routing with BIN-based or dynamic strategies

- Strengthen fraud prevention to lower risk-based fees

- Verify your Merchant Category Code (MCC) for accuracy

- Include Level II/III data to qualify for lower interchange rates

- Use delayed capture to avoid unnecessary refund costs

- Regularly monitor your payment data to uncover savings

- Allocate all fees and costs on a transactional level to spot transactional cost anomalies

These are just some of the ways to optimize payment costs. In future posts, we’ll dive deeper into each strategy—stay tuned.

Reduce your payment fees with Congrify

Understanding your payment fees is one thing—actively managing them is another. That’s where Congrify comes in.

With Congrify’s payments intelligence and observability platform, you get a solution that dives deep into multiple data dimensions and allocates every cost to a specific category, enabling immediate and actionable analysis.

From meticulous cost breakdowns to granular insights into interchange, scheme, processing fees, and more, we help Finance, Operations, and Payments teams align around a single source of truth—and unlock savings where it matters most.

👉 Ready to uncover hidden costs and improve your payment performance? Let’s have a chat!

Note:

This article is just the beginning. In our upcoming posts, we’ll break down each major fee—interchange, scheme, acquirer, gateway, and more, to help you fully understand what you’re paying and why.

Follow us to stay updated!